Iris Energy: Reasonable And Renewable Play On Bitcoin (NASDAQ:IREN)

alvarez

The Basic Thesis

Anyone who has followed my writing knows that I am not a fan of most Bitcoin and other cryptocurrency plays. To the extent one wants exposure to cryptocurrencies, I believe companies like Coinbase (COIN) and MicroStrategy (MSTR) are horrendous and inefficient pathways with bad business models, sketchy balance sheets, and worse management teams.

I also have had a generally healthy skepticism of Bitcoin (BTC-USD), no surprise for a value and credit guy. That said, if the first rule of investing is “Don’t lose money” and the second is “Don’t forget rule #1”, the third is “stay humble and open-minded.” Bitcoin has had an awful lot thrown at it and is still around.

Since I do not intend to abandon my short views on COIN and MSTR, a long on the other side is almost necessary. Fortunately, Iris Energy is a play on Bitcoin with good core economics, a solid balance sheet, top-notch management, and downside protection from asset flexibility.

Iris Energy (NASDAQ:IREN) is the largest Nasdaq-listed Bitcoin miner using 100% renewable energy. It provides an attractive “data center” exposure to the Bitcoin theme by combining:

- leading high-efficiency data centers designed and built in-house

- operations powered by low-cost, excess renewable energy.

These virtues lead to ~$200m high margin illustrative annualized mining profit in the current market (revenue minus assumed mining pool fees) and low assumed electricity costs ($0.045/kWh is based on existing BC operations). Together these advantages mean significant expected cash generation on top of a strong balance sheet ($55m cash, no debt) and a low-risk growth opportunity.

Iris Bitcoin Mining Assets

Iris Energy currently has three operating sites in British Columbia, Canada (Canal Flats, Mackenzie and Prince George) and one site recently completed in Childress, Texas, which currently supports 5.5 Exa Hash/second (or 180MW) of computing power. For the uninitiated, you can find an explanation of exa hash and hashrate here.

Iris Energy builds and operates its own proprietary data centers, providing long-term security and operational control over its assets. The Company’s facilities are regularly ranked amongst the most efficient in the industry in terms of uptime.

The company recently announced an additional plan for 1.0 EH/s near-term expansion at its Childress site without raising any additional capital. This will put Iris as the 4th largest self-miner in the world.

|

Site |

Capacity (MW) |

Capacity (EH/s) |

Status |

|

Canal Flats (BC, Canada) |

30 |

0.8 |

Operating |

|

Mackenzie (BC, Canada) |

80 |

2.5 |

Operating |

|

Prince George (BC, Canada) |

50 |

1.6 |

Operating |

|

Total (BC, Canada) |

160 |

4.9 |

|

|

Childress (Texas, USA) |

20 |

0.6 |

Operating |

|

Total (Canada & USA) |

180 |

5.5 |

|

|

Childress (Texas, USA) |

600 |

~18 |

Additional expansion capacity |

Iris Energy Advantage

Iris Energy has used 100% renewable energy since its inception. The Company targets markets with low-cost, excess renewable energy where its operations can help solve energy market challenges (e.g. contributing to lower power prices in regulated energy markets such as British Columbia or shedding load to support deregulated energy markets with high penetration of intermittent renewables such as Texas).

Not only does this strategy give Iris cheap energy, it also helps mitigate potential regulatory and/or political risks associated with its operations.

Iris Energy’s cost of power for its BC operations as of March 2023 was ~$0.045/kWh (or ~$11.5k per Bitcoin vs. current spot price at the time of this writing of ~$26k/coin). Importantly, the Company’s cost of power in BC is reviewed and fixed on a 12-month basis, providing certainty across its projects.

The Company recently disclosed that as part of BC Hydro’s annual rate review, its all-in unit cost of power was expected to increase by ~2% for the fiscal year commencing April 1, 2023 (i.e. an increase of ~$0.001/kWh).

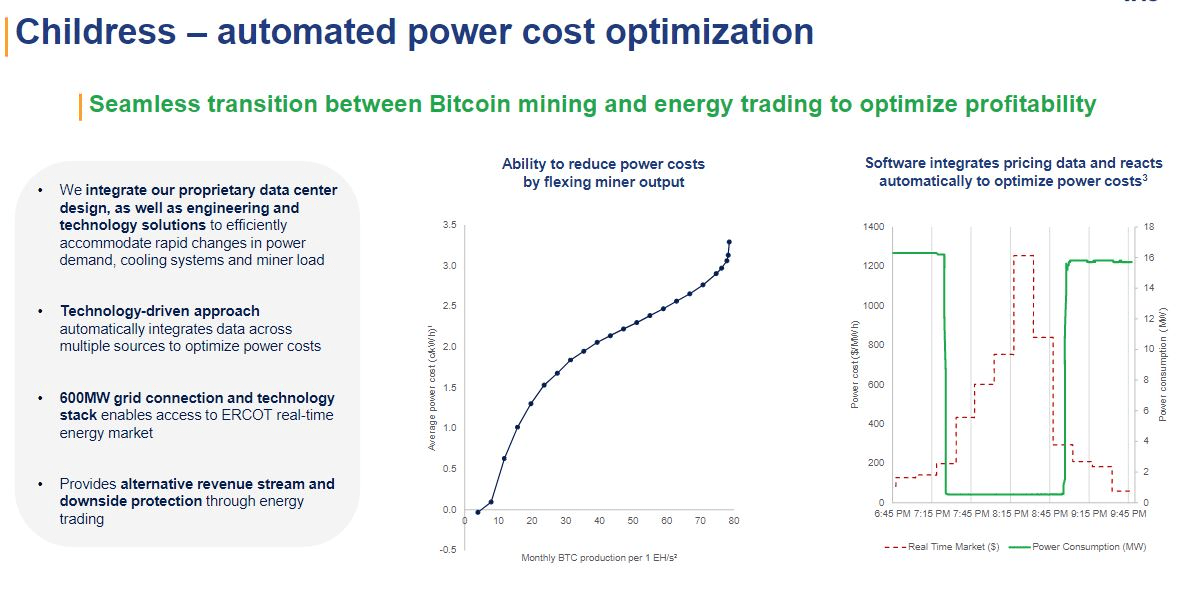

The company also has low-risk and near-term growth opportunities at its Childress site (600MW of potential expansion capacity).

It has made significant upfront investments in key infrastructure (such as the 600MW bulk power substation and the first 100MW primary substation) which provides the ability to rapidly and efficiently scale beyond the Company’s initial 20MW data center.

The Childress site bulk power station is connected to the ERCOT grid, allowing real-time access to spot prices in the energy market. To fully utilize that connection, the Company has an integrated proprietary data center design with engineering and technology that rapidly change power demand, cooling system, and miner load – effectively maximizing cost per kWH.

Childress Power Optimization (Iris Energy Q1 Presentation)

Significant cash generation and margins

The Company’s 5.5 EH/s of capacity can generate strong cash flows in the current market with upside leverage to increases in Bitcoin’s price. I’ll also note here that Iris Energy has a non-HODL strategy (it liquidates all Bitcoin mined daily). This strategy provides a lower risk, “cash flow” exposure to Bitcoin.

|

Bitcoin price (US$) |

$20,000 |

$30,000 |

$40,000 |

$50,000 |

|

Revenue |

$107mm |

$160mm |

$213mm |

$266mm |

|

Mining profit |

$40mm |

$93mm |

$146mm |

$199mm |

|

Site & corporate costs |

$24mm |

$24mm |

$24mm |

$24mm |

Iris plans to add an incremental capacity of 1.0 EH/s of miners at its Childress site in Texas, which would obviously increase the numbers above. Childress currently has 20MW of operating capacity with near-term plans to add an additional 20MW. The company estimates the 1.0EH expansion will require ~$35mm of CapEx spending. Given that the company has $55mm of cash plus strong operating cash flow, it can fund its near-term expansion without additional capital. Most other miners, such as Marathon (MARA), do not have this ability.

Moreover, management speaks repeatedly that any future growth capex would have to be accretive nearly day one. Therefore, I will assume that should any growth opportunities arose that could not be funded internally, the same accretive hurdle would apply to any debt and/or equity funding.

Valuation and Comps

Iris Energy is positioned favourably when compared to its listed peers across key metrics, including:

- power source (100% renewable energy)

- geographic diversification

- efficiency (BTC mined per EH/s installed).

Despite these advantages, the Company continues to trade at a material discount compared to its peers on both an EV/EH and EV/EBITDA basis, which vary widely between comps.

|

IREN |

Marathon Digital (MARA) |

Riot Platforms (RIOT) |

CleanSpark (CLSK) |

Hut 8 Mining (HUT) |

Cipher Mining (CIFR) |

|

|

100% renewables |

Yes |

No |

No |

No |

No |

No |

|

Geographies |

Canada, USA |

USA |

USA |

USA |

Canada, USA |

USA |

|

Efficiency (BTC per EH/s) |

113 |

83 |

77 |

108 |

89 |

81 |

|

Hashrate (EH/s) |

5.5 |

11.5 |

10.5 |

6.7 |

2.6 |

5.7 |

|

NTM Est’d EBITDA ($mm) |

26 |

169 |

84 |

69 |

n/a |

n/a |

|

EV ($mm) |

162 |

2,102 |

1,693 |

505 |

539 |

516 |

|

Multiple (EV/EH) |

29 |

182 |

161 |

75 |

206 |

90.5 |

|

Multiple (EV/EBITDA) |

6.3 |

12.5 |

20.1 |

7.3 |

n/a |

n/a |

Management

Unlike COIN, whose management is in a tiff with the SEC, and MSTR whose management is running away from a garbage software business by throwing a crazy leveraged hail Mary on Bitcoin, Iris Energy is led by a seasoned management team with an impressive track record of success across renewables, infrastructure, and digital assets, having delivered tens of billions of energy and infrastructure projects globally. The Company’s founders, board, and management own approximately 23% of the Company’s shares, promoting long-term alignment of interest.

Risks

The main risk with any cryptocurrency-tied company is the decline in values of coins. I believe that Iris mines Bitcoin profitably down to ~$18,000/coin.

However, because Iris has such modern and energy-efficient operations, it could convert those facilities to other uses, such as data centers, if Bitcoin prices plummeted significantly below $20,000 and stayed there. Management has never given a concrete number of what that transition would cost, but the balance sheet should give them the flexibility to execute an alternate use. Another alternative could be selling their facilities to another company for use as a data center.

One more risk is that the company goes against what they have indicated about accretive versus dilutive equity. Any equity (or debt for that matter) that was seen as dilutive (short or long term) could knock the stock down. Ultimately, I think management is highly unlikely to a dilutive offering of any kind, but miners often need capital and a potential offering that is or could be perceived as dilutive is a risk everyone should be aware of.

Conclusion

As I said at the beginning of this piece, my main issue with cryptocurrencies is finding a reasonable way to invest in them. In my opinion, Iris Energy provides an attractive approach. It has a liquid, net-cash balance sheet and a significant real asset base that generates cash flow mining Bitcoin down to ~$18,000/coin, in my estimates.

The Company’s leading high-efficiency data centers and renewable energy strategy are key differentiators from its listed peers, as is its ability to convert to data centers if Bitcoin mining disappears. The imminent installation of the Company’s 6.5 EH/s of capacity and low-risk, near-term growth opportunity at Childress (600MW of potential expansion capacity) are also positive catalysts.

I think Iren can easily double from here and perhaps much more when one looks at the valuations of comps. It is an excellent long against Coinbase and MicroStrategy or other miners. That said, all positions in cryptocurrencies are inherently extremely volatile and speculative. Consider the stock’s volatility plus that of Bitcoin and the lack of testing of long-term value of cryptocurrencies before making any investment, long or short.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.