Miners Are Biggest Risk Facing Bitcoin Price – Bitcoin Magazine

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

As Hash Rate Soars, Parallels to 2018 Arise

On October 23, bitcoin mining difficulty saw an upwards adjustment of 3.44% (after the previous adjustment of 13.55%), pushing mining difficulty to yet another all-time high as hash rate continues to soar. With the price of bitcoin stagnating at $20,000 give or take for the last few months, we have noticed some parallels between the market cycle of 2018 and the one in front of us today.

Meme Source: Braiins Mining

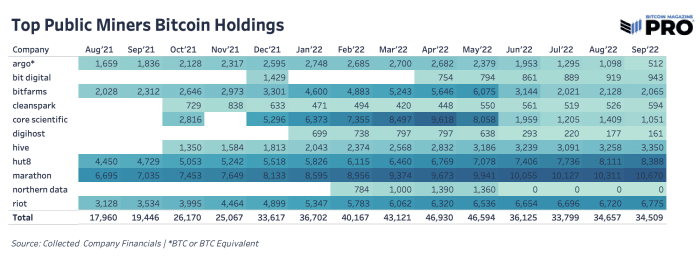

The rising hash rate dynamic seen throughout 2022 while the bitcoin price has fallen has put a lot of pressure on both public and private mining operations. Throughout the year, we have seen public miners capitulate on their bitcoin holdings, as diminishing revenue and treasury values have placed increasing pressure on balance sheets.

At their peak, public miners’ bitcoin holdings reached over 46,000 BTC but have since fallen 26% as bitcoin treasuries were sold out of necessity to access more capital, pay down debt and fund operations and expansion plans. Although estimated and rough numbers, the top public miners make up over 20% of all Bitcoin’s network hash rate. Moves from public miners to not only sell bitcoin holdings but also to expand and contract their hash rate have a significant impact on the market.

Bitcoin holdings from the top publicly traded bitcoin mining companies

As hash price continues to trend to all time lows, the probability of a miner capitulation/liquidation event probabilistically increases until a drawdown in hash rate, as certain entities cease mining and liquidate their assets (in the form of both bitcoin and ASICs).

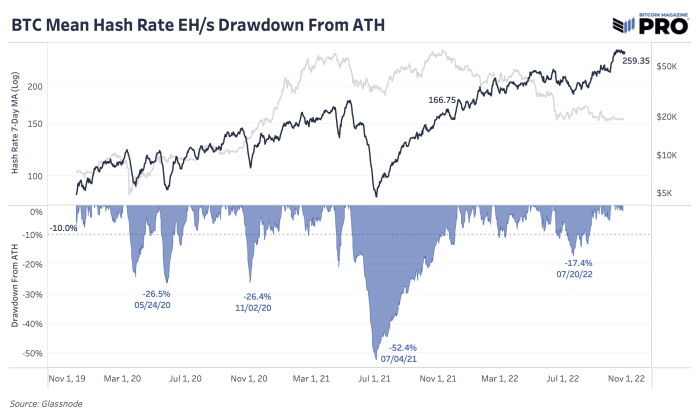

Barring the China mining ban during 2021, the largest peak-to-trough drop in hash rate (7d MA) in the history of bitcoin was approximately 35%. In our opinion, this bear market cycle won’t end until a flush of the weakest miner participants has occurred, which will be observable by a temporary yet meaningful fall in hash rate and will subsequently decrease mining difficulty, easing conditions for the surviving participants.

While there was already a “capitulation” per se earlier this summer during the initial cryptocurrency market deleveraging in June, hash rate has since gone vertical, with new fleets of the newest Bitmain Antminer S19 XP, an industry-leading miner, just now being deployed en masse by the largest miners.

Given the current state of hash rate and difficulty, we believe that the pressure is indeed building, but the figurative burst has yet to occur.

The Mechanics Of A Race To The Bottom

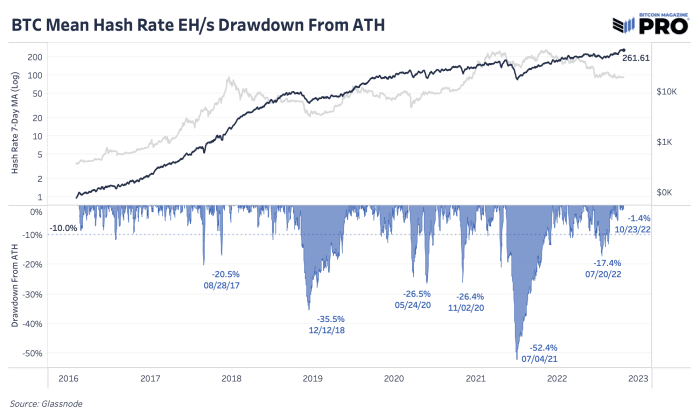

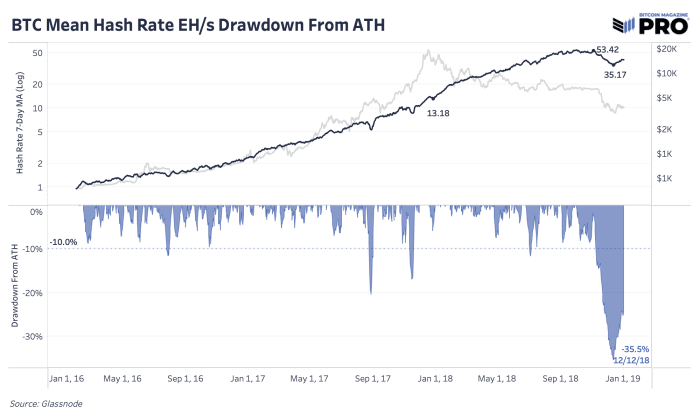

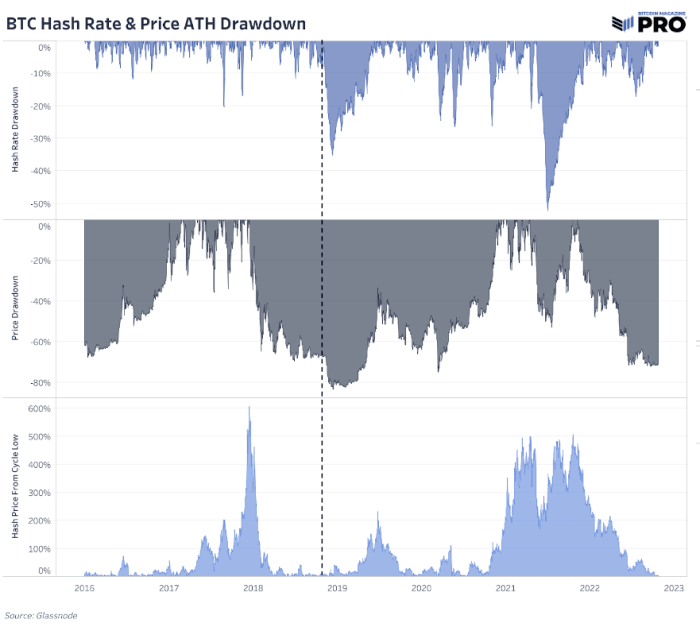

We could easily see a scenario where further bitcoin price and miner industry revenue pressures force more of that held bitcoin back into the market along with a significant drawdown in hash rate. Below charts show the comparison of hash rate, price trajectory and percentage drawdown from 2018 and present day.

The comparison of hash rate, price trajectory and percentage drawdown from 2018

The current comparison of hash rate, price trajectory and percentage drawdown

If there is a case for the last last leg lower, this is it, and our data-driven approach has us leaning towards this having a decent likelihood of playing out. In the chart below, observe what happened to the bitcoin market the last time there was a price stagnation following a drawdown of this caliber as hash rate soared to daily new highs (hint: the dotted line).

The last time there was a price stagnation following a major hash rate drawdown

While history doesn’t repeat, it often rhymes, and our data-driven approach has our team on increasing alert about the pressure this mining industry and subsequently the bitcoin market will face over the short term.

While we are in no way saying this occurs with certainty, the higher that hash rate goes while bitcoin the asset itself trades with increasingly muted levels of volatility -71% from its previous all-time high (around when some of the largest CapEx investments made into mining infrastructure took place), then it is increasingly probable a final miner-induced capitulation event will occur. This is not a prediction, but rather an observation based on the data currently in front of us.

Relevant Past Articles: